SME Financing Readiness Guide

Term Loan vs Overdraft: Which Is Better for Your Business?

A term loan and an overdraft can both support Malaysian SMEs, but they are not meant for the same financial situation. The better choice depends on your cash flow cycle, repayment ability, funding purpose and how predictable your business needs are.

Quick Answer

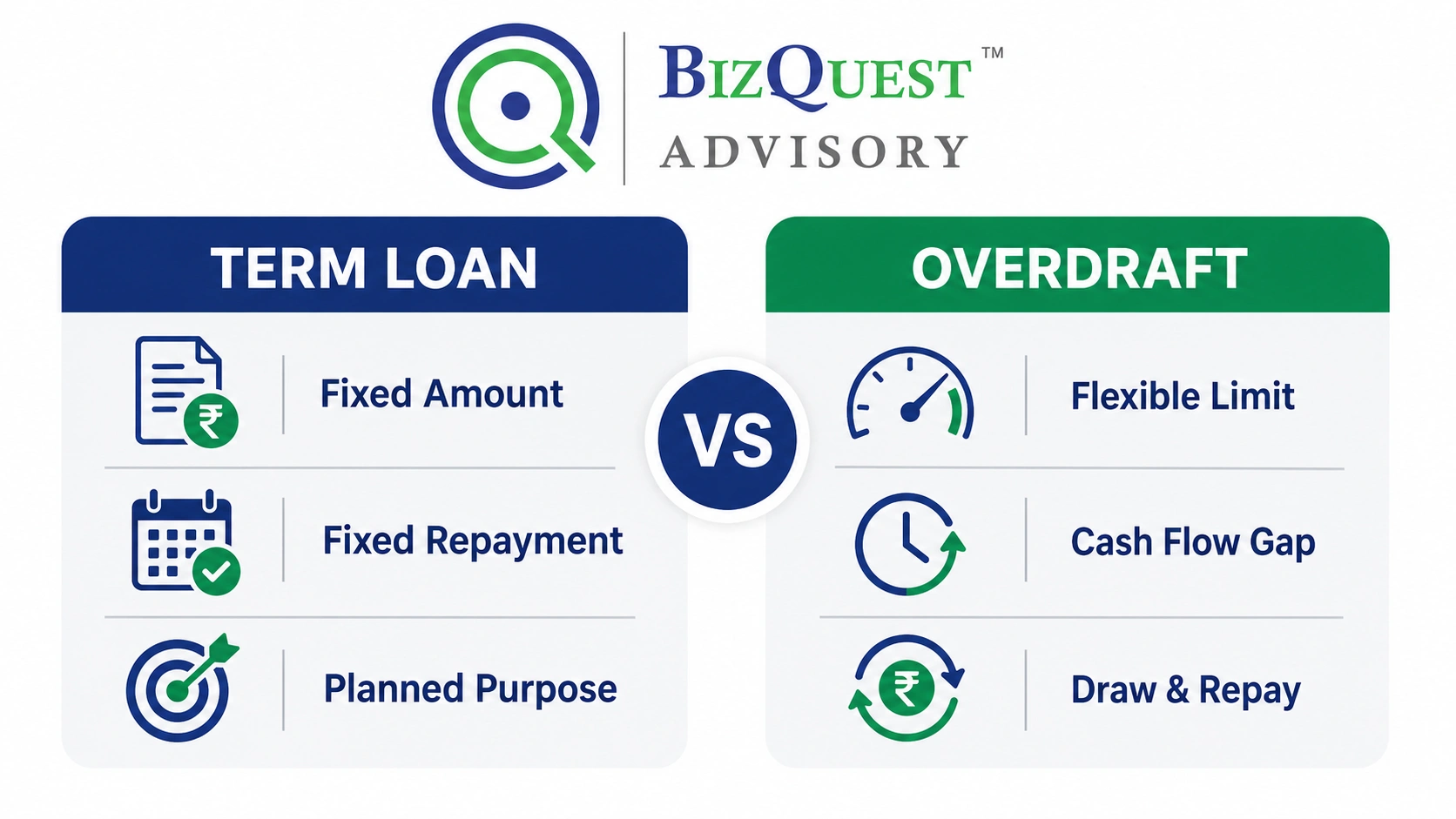

A term loan is usually more suitable for planned, fixed business needs such as expansion, machinery, renovation, project setup or structured working capital.

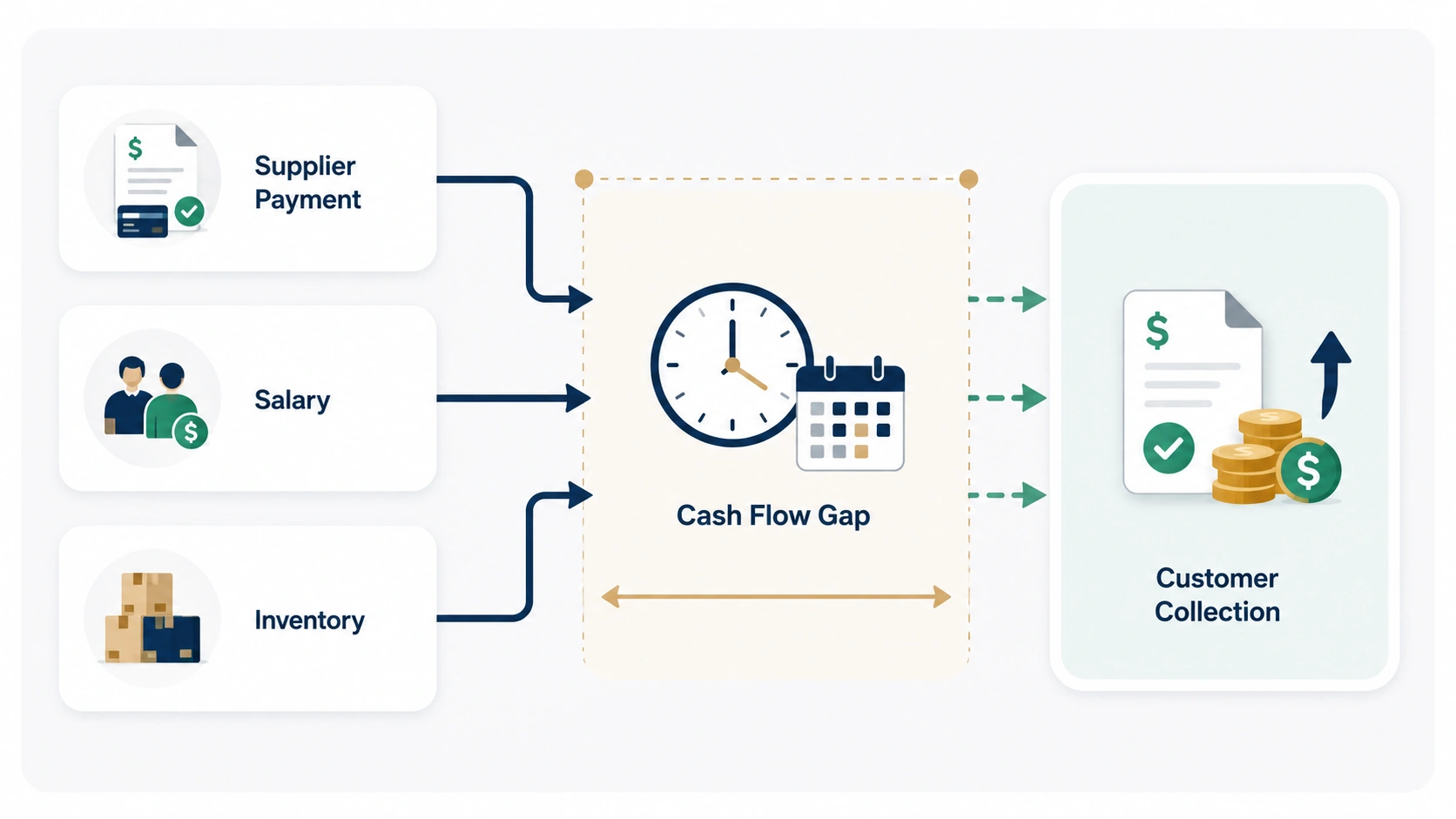

An overdraft is usually more suitable for short-term cash flow gaps where the business needs flexible access to funds due to delayed customer payments, supplier timing differences or temporary working capital pressure.

The best choice is not only about interest rate. It depends on whether the facility matches your actual business cash flow and repayment pattern.

Why Malaysian SMEs Compare Term Loan vs Overdraft

Many SME owners search for term loan vs overdraft when they need financing but are unsure which facility fits their business. Both can provide funding, but they work differently.

Some businesses need a fixed amount for a planned purpose. Others only need temporary cash support when customers pay late or when supplier payments come before sales collections. Choosing the wrong facility can create unnecessary repayment pressure, even if the business is still profitable.

BizQuest perspective: before choosing any financing option, SME owners should first understand their cash flow position, working capital cycle and repayment ability. Financing should support the business, not hide a deeper cash flow problem.

What Is a Term Loan?

A term loan is a financing facility where the business receives an approved amount and repays it over an agreed period. Repayment is usually structured through fixed monthly instalments or a defined repayment schedule.

For SMEs, a term loan may be used for planned business needs such as business expansion, equipment purchase, renovation, inventory build-up, project preparation or longer-term working capital support.

When a term loan may be suitable

- The business has a clear funding purpose and knows how much is needed.

- The repayment can be supported by predictable business cash flow.

- The financing need is not just a one-off timing gap, but a planned investment or structured business requirement.

- The business owner wants a clear repayment timeline instead of flexible drawings.

What Is a Business Overdraft?

A business overdraft is a revolving credit facility linked to business cash flow needs. Instead of receiving one fixed lump sum for a fixed purpose, the business can draw from the approved limit when cash is needed and reduce the outstanding amount when collections come in.

This type of facility can be useful for businesses with temporary cash flow mismatches, especially when sales are healthy but collections are delayed.

When an overdraft may be suitable

- The business has short-term cash flow gaps due to delayed customer payments.

- The business needs flexible access to funds, not a full lump sum upfront.

- The cash shortage is temporary and expected to recover through confirmed collections.

- The business has discipline to use the facility for working capital, not uncontrolled spending.

Term Loan vs Overdraft: Key Differences for SMEs

The right comparison is not simply “which one is cheaper”. SME owners should compare how each facility fits the business purpose, cash flow behaviour and repayment discipline.

| Area | Term Loan | Overdraft |

|---|---|---|

| Main Purpose | Planned financing for expansion, equipment, project cost, renovation, inventory or structured working capital. | Flexible short-term support for cash flow gaps, delayed collections or temporary working capital needs. |

| Fund Access | Usually disbursed as an approved amount based on facility terms. | Draw from the approved limit when needed and reduce usage when cash comes in. |

| Repayment Style | More structured, usually with a fixed repayment period or monthly commitment. | More flexible, but requires strong discipline to avoid long-term dependency. |

| Best For | Predictable needs with a clear purpose and repayment plan. | Timing gaps between outgoing payments and incoming collections. |

| Cash Flow Impact | Creates a regular repayment commitment, so cash flow must support instalments. | Can support liquidity, but poor control may keep the business constantly near its limit. |

| Risk to Watch | Borrowing more than the business can repay from actual cash flow. | Using short-term credit to cover deeper profitability or collection problems. |

Which Is Better for Your Business?

There is no single answer for every SME. A term loan may be better when the business has a fixed need and a clear repayment plan. An overdraft may be better when the business has temporary cash flow gaps and needs flexibility.

Choose a Term Loan When...

Your business needs a planned amount for a specific purpose, such as machinery, renovation, business expansion, project setup or a structured working capital requirement.

A term loan may also be easier to manage when you want a fixed repayment structure and can forecast the business cash flow clearly.

Choose an Overdraft When...

Your business has sales and confirmed collections, but cash comes in later than expenses go out. This can happen when customers take 30, 60 or 90 days to pay.

An overdraft may help bridge timing gaps, but it should not replace proper cash flow management.

Practical rule: use a term loan for planned funding needs. Use an overdraft for temporary cash flow timing gaps. If the business has weak margins, poor collections or unclear financial records, review the numbers before applying for either option.

What SMEs Should Check Before Choosing a Facility

Before comparing facilities, business owners should understand whether the business is financially ready. The wrong financing structure may increase pressure even when sales look strong.

Review your cash flow cycle

Check how long it takes to collect from customers and how quickly you must pay suppliers, salaries, rent, utilities and other commitments.

Understand your funding purpose

Be clear whether the funds are for working capital, inventory, expansion, equipment, project cost or short-term cash flow support.

Check repayment ability

A facility is only useful if the business can support repayment without damaging daily operations.

Review receivables, payables and inventory

Trade receivables, trade payables and inventory often explain why a business has sales but limited cash available.

Prepare proper financial records

Clear financial statements, management accounts and bank statement patterns can help business owners understand their position more realistically.

For a more structured check, explore BizQuest’s Working Capital Analysis or try the Free SME Cash Flow Calculator before deciding which facility makes sense.

Common Mistakes When Choosing Between Term Loan and Overdraft

Many financing problems happen not because the facility is bad, but because the facility does not match the real business issue.

- Using a term loan for unclear spending: Borrowing a fixed amount without a clear business purpose can create repayment pressure.

- Using an overdraft like permanent capital: An overdraft is meant for flexibility, but long-term dependency may signal deeper cash flow issues.

- Ignoring customer payment delays: If collections are slow, the business may need to fix receivable management, not only add financing.

- Focusing only on approval: Getting financing is not the end goal. The facility should improve the business position.

- Applying without financial clarity: SME owners should understand their cash flow, commitments and repayment ability before applying.

How BizQuest Can Help SMEs Compare Financing Options

BizQuest Advisory helps Malaysian SMEs understand their financial position before making financing decisions. This includes reviewing cash flow, working capital structure, funding purpose and financing readiness.

If you are unsure whether a term loan, overdraft or another facility is more suitable, the smarter first step is to understand your numbers. The right facility should match your business cycle, not just your immediate cash need.

BizQuest does not encourage SMEs to borrow blindly. The focus is to help business owners make clearer, more responsible financial decisions before applying for funding or injecting new capital.

Related guides: Working Capital Loan Malaysia, What to Do If Your SME Loan Is Rejected, and Capital Injection Profitability Analysis.

Not Sure Which Financing Option Fits Your Business?

Before choosing between a term loan and an overdraft, review your cash flow, working capital position and repayment ability. BizQuest can help you understand your numbers more clearly so your next financing decision is based on facts, not guesswork.

Frequently Asked Questions

Is a term loan better than an overdraft for SMEs?

A term loan may be better for planned business needs with a clear amount and repayment plan. An overdraft may be better for short-term cash flow gaps where flexible access to funds is needed.

When should a business use an overdraft?

A business overdraft may be suitable when the company has temporary cash flow timing gaps, such as delayed customer payments or supplier payments due before collections come in.

When should a business use a term loan?

A term loan may be suitable when the business needs funding for a planned purpose such as expansion, machinery, renovation, inventory, project costs or structured working capital.

Can an overdraft solve long-term cash flow problems?

Not always. An overdraft can help with short-term liquidity, but if the business has weak margins, slow collections, high commitments or poor financial control, those issues should be reviewed first.

What should SMEs check before applying for a term loan or overdraft?

SMEs should review cash flow, receivables, payables, inventory, existing commitments, bank statement patterns, financing purpose and repayment ability before choosing a facility.

How can BizQuest help me choose between a term loan and an overdraft?

BizQuest helps SME owners review their financial position, understand working capital needs, assess repayment ability and make more informed financing decisions before applying.